Message Monday: Should Christians Invest in Peer-to-Peer Lending?

Peer-to-Peer lending is all the rage these days. It is a way for someone to loan another individual money over the internet, a concept that hadn’t existed before. Should Christians invest in peer-to-peer lending? I give my opinion on why Christians should not invest in peer-to-peer lending and suggestions on how they can help the needy.

Peer-to-Peer lending is all the rage these days. It is a way for someone to loan another individual money over the internet, a concept that hadn’t existed before. Should Christians invest in peer-to-peer lending? I give my opinion on why Christians should not invest in peer-to-peer lending and suggestions on how they can help the needy.

Peer-to-peer lending is enables financial misbehavior

Lending money to someone, especially on the internet without a personal connections, does not solve the problem. Someone with thousands of dollars in credit card debt had a problem with overspending, not interest rates.

For example: One customer of a peer-to-peer lending site said “Getting engaged forced me to make some important financial decisions“. That is a good thing. His actions will affect his future spouse’s life. However, he continued with “so I consolidated several sources of debt with a single loan from Lending Club“.

Yes, lowering an interest rate through a peer-to-peer loan could lessen the monthly burden, but it does not pay off the debt. Borrowing money from a different source, such as peer-to-peer lending sites, could be hiding the problem, not solving it.

Instead, teach people financial responsibility. Show them how to budget or teach them how the envelope system works. Have them attend Financial Peace University or other financial literacy class. If you don’t know the person then why are you lending him/her money through peer-to-peer lending?

Don’t lend someone a “peer-to-peer fish”, teach them how to fish instead.

Learn how to spend purposefully and get control of your money

Investing wisely is not about making money off the needy

Everything comes from God and we are called to be wise stewards of His money. Earning interest is fine, but I have to question the method of how that interest is earned.

Putting the money into a savings account or online Money Market account will earn simple interest through banks. Investing in stocks or mutual funds is purchasing pieces of companies that are growing (or, conversely, dying).

However, expecting to earn interest on the loans made to individuals through a peer-to-peer lending site is making interest off of the needy. How do I know they are needy? If someone were able to borrow money from a bank or relative then they wouldn’t need a peer-to-peer lending site.

“Love thy neighbor as thyself” – Matthew [22:39] convinced me to look closer at my investments. Peer-to-peer lending just doesn’t fit my integrity model.

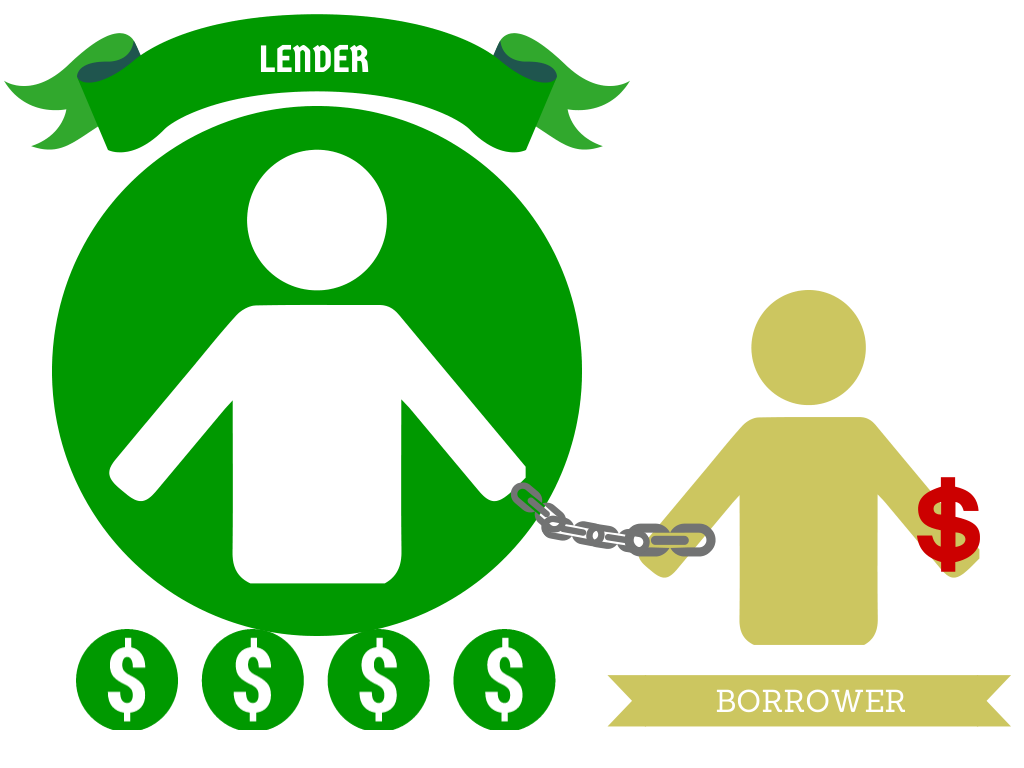

Peer-lender -to- pure-slave

The rich rule over the poor, and the borrower is slave to the lender.

Proverbs 22:7 says it clear as day! I am not a bank, I am a human being. If my brother comes to me for money I should not have him sign 35 pages of loan documents promising a set interest rate to be paid back in xx-months, I should give him my shirt.

Anyone who has two shirts should share with the one who has none, and anyone who has food should do the same. – Luke [3:11]. I do not wish to make my brother my slave, so lending to an individual is no longer in my vocabulary.

Giving money can be much more effective than lending. A peer-to-peer lending site doesn’t know how your “investment” is used but you have input on how your money can help someone in need.

BTW: If I have the ability to participate in a peer-to-peer lending site then I am able to give instead. Otherwise I shouldn’t be risking the money in this manner.

Peer-to-peer lending websites can give you a better interest rate on the money you contribute, but at what cost? A believer should consider who is being affected by this type of investment and the side-effects of their actions. I have been tempted to invest some of our emergency fund in a peer-to-peer lending site because of the higher returns.

It was only after talking to someone who had used peer-to-peer lending that I realized I wasn’t really helping anyone. I was enabling them to manage their debt instead of eliminate it. As a Christian, I’d rather teach them how to pay attention, not interest through a peer-to-peer lending site.

I agree with your blog. However, there are some sites that lend at Zero percent interest rate – for example kiva.org. So instead of having my money in the bank being lent to I do not know who I could potentially help out some small farmer with zero per cent interest loan. What I would like to find is some Christian site that does this.

That’s an interesting thought Tom. You are right, money saved in a bank gets lent out to others at a higher interest rate.

Can you get money out of Kiva.org quickly? If so then this would be a good use for extra cash that ins’t needed right away. (Note: I don’t believe this would include your emergency savings, that has to be very liquid). How much money do you have in Kiva.org?

I am wondering about this issue currently, On the one hand I agree there are problems with loans etc, but ready access to money can be extremely helpful for people, and peer to peer lending is at a better rate than the bank offers, if the person needs money anyway why not cut out the middle man.

I think the article’s argument is short sighted and leagalisitic. What do you think happens with your money when you lend it to a bank? They turn around and lend it to individuals whom they gouge. The whole reason p2p lending is taking off is because it’s cutting out the middle man, and thereby helping both sides by reducing the over head of the lending institution. If you don’t believe in loaning money to individuals then you don’t believe in interest at all. Because all interest is derived from loans. The vast majority issued to individuals. (Notice, interest is different than a return, such as what you might make on the stock market or other investment.)

Also, not all loans are created equal. Some loans might be for essentials, like food and clothes, which I agree as Christians we should simply meet these needs. Some times they are for assets such as cars or houses, or for investments like venture capital. Obviously we aren’t called to give people houses and cars, especially to those people who can provide for their selves. Also, if you finance a business venture, even to an individual (verses a group) don’t you have a stake in that business, you are investing your time/work/effort in for form of money (as you had to spend those things to get money) shouldn’t you see a return, just like the man who is working to build that business?

Also, if you persist in that Christians shouldn’t issue loans for any reason, then it is equally true that Christians shouldn’t take loans for any reason. As we are making another person sin.

Now I personally feel that there is a proper time and place to loan and barrow money, and there is an improper time and place. If you are operating within the proper guidelines then you are acting honorably and wise. Most anyone who thinks about it will agree that it makes sense to barrow money to buy a house, because otherwise you will have to spend that money to rent, while you are tying to save the money to buy a house.

I think it would be foolish indeed to argue that you simply should abstain from barrowing, which means some one must lend, and likewise it therefore can’t be good to do one and evil to do the other. …and hiding behind a burocrocy like a bank does not alleviate your cupribility. In fact, I’d say the main advantage of p2p is it gives you more control of what sort of loans you fund, instead of a bank who will simply use your money however they see fit.

James makes some very good points.

I do believe we should give instead of loan to another and we should teach people how to be better financial stewards rather than search for ways to reduce their interest rates.

One final comment I would add is the BIble clearly states the borrower is slave to the lender (Proverbs 22:7). It does not state that it is a sin – and I wasn’t trying to say that in this article – but it certainly doesn’t put a positive spin on taking out loans.

Steve, I’m glad to hear that you aren’t positioning yourself with the argument that it is a “sin” to barrow/loan money. Though, honestly, I feel like you are skirting the issue. A sin is anything that isn’t pleasing in the eyes of the Lord. So even though you haven’t come out and said it’s a sin, you have implied it with statements like, “…but it [the Bible] certainly doesn’t put a positive spin on taking out loans”. Which, as we’ll get to later, is just that, spin, and spin is in the eye of the beholder, whereas a sin is something that is concrete. Like “do not lie”, is a command, if you break it, you have sinned, period, nothing subjective about that.

I think the whole question of whether or not you should give or loan really has to do with what is being discussed. I mean the Bible also clearly teaches we should strive not to be a burden, that if a man will not work nor should he eat (2 Thessalonians 3:10). There is also a clear need to have shelter. Now let’s say Joe is making $40k a year, does he pay $600 a month in rent, and try to save as much as he can on the side, till he can afford a $130k house in cash, or does Joe get a lone for a $100k with a payment of $575.66 (at 5.6.25 percent at 30 years, what my rate is, and Joe could do even better with a $30k down payment)? Bear in mind as well that rent could always go up, whereas a loan (if you’re wise) is set. Obviously Joe wouldn’t be wise with his resources (something he’s commanded to be) to be paying in rent what he could pay to own!

Now that we have identified that 1) Joe can afford to provide for himself 2) that he has a responsibility to provide for himself 3) that it would be more wise for him to get a loan than to rent (rent is really just another form of debt if you think about it), then that leads to the next question: Let’s say Bob also makes $40k a year and has managed to save a $100k, is Bob obligate to give Joe that $100k to meet Joe’s obvious shelter need so that Joe can avoid “becoming a slave”? Obviously not! There is no reason to meet another man’s need that that man is in the position to meet for himself! …additionally it’s not wise, and it’s against Biblical principles (think back to 2 Thessalonians 3:10).

The reality here is that we are all slaves. If we are Christians we are slaves to the Lord first and foremost. But all men have servitude to pay to survive in this material world. Additionally there were Christian slaves and masters recorded in the New Testament. Also Proverbs is just that, proverbs. Proverbs is wise counsel; it’s not some sort of rigorous theological doctrine. Proverbs 22: 6 states: “Train up a child in the way he should go: and when he is old, he will not depart from it.” (KJV) Obviously this isn’t a guarantee that your child will be a Christian just because you raise him to be one. But in general, good parenting has a profound impact on children’s lives, and it should not be neglected. Likewise, in general, debt is bad, but there are times that it is unwise to avoid it. But the overall point is that you should think long and hard before you decide to go into debt.

Now that we have some foundation let’s talk about p2p lending again, the main topic here. It was suggested in the article that it’s ok to loan your money to a bank, and thereby to gain interest that way, because you aren’t loaning to an individual. But conversely it’s not ok to use p2p lending to invest your money because you are loaning to an individual and therefore you are making him a slave.

1) When you loan to that bank (the slave master) you are enabling that bank to make loans (to create slaves). So if you are against this, you should not keep your money in banks, period. You should also not purchase loans from them. Just defund the situation entirely.

2) The p2p situation is materially the same as loaning to a bank. You are not really loaning to an individual, you are loaning to Proper or Lending Club or what have you, they in turn are lending to the individual, so if you feel comfortable with the level of abstraction provided by the bank to make it ok, you should feel equally comfortable with the p2p arrangement. Moreover, there is a practical point to this as a well, seeing as you aren’t loaning to the individual you have zero recourse to take against that individual should he default. So he really isn’t your slave. Now if you feel bad that you enabled his slavery by funding the loan, then you should really go back and read point one again.

3) We have already established there are legitimate reasons to have loans, therefore there are legitimate reasons to issue loans, and therefore it’s right and proper to make them. That means that it’s incumbent on the barrow to know whether or not it’s right for him to take that loan. Which is exactly the way Proverbs 22:7 is written. It’s not with some sort of moral imperative, but rather it’s simply an observation of a relationship. It’s up to the reader whether or not they wish to enter into that relationship, and it would seem the slave has the most to lose (his freedom), thus he would be wise to think carefully indeed. There is nothing morally right or wrong about being a master or a slave, even though in 21st century America that relationship has very negative overtones to it. Sometimes you have to be careful not to read your own culture into what the Bible is telling you.

One other thing, you have some misinformation in your main article:

“How do I know they are needy? If someone were able to borrow money from a bank or relative then they wouldn’t need a peer-to-peer lending site.”

In order to get a loan from Prosper you are requires to have a minimum FICO score of 630, to get a loan from Lending Club you are required to have a score of 640. This puts you in what is considered prime, any lending institution is happy to lend to you. So your argument that the fact they are on a p2p site shows they are “needy” is wrong, it’s not just wrong, it’s deed wrong. People don’t have 600+ credit scores because they are needy, they have 600+ credit scores because they have proven to be responsible with their credit (in so much as they pay their bills). In order to have that score you have to have been meeting your obligations, which means they aren’t “needy”, they aren’t in the poor house looking for where to find food. There are other such errors in your article. However, beside the arguments I have brought to date, I think you need to reexamine many of your base assumptions.

Also I would personally rather barrow money from an institution (which all the “p2p sites” are) that from a relative. I don’t want to risk poisoning a relation that’s important to me. Regardless of your intentions, things can always happen that result in your being insolvent. I would not want that to be hanging between me and family. This goes back to that verse you like to point out, Proverbs 22:7, and that’s not a relationship I want with family. Though I will be on either side of it with a stranger.

True, I can’t prove that someone using Peer-to-Peer lending is “needy”, but if we are borrowing money couldn’t we say we justified the purchase of something we “wanted” but don’t truly need?

I don’t have to buy a house but I do need shelter. There are people and places who can help with that.

I don’t have to have new clothes but if I need to cover my body with something there are more frugal ways to acquire coverings and charities that will donate to us (Woman’s Another Chance comes to mind and our church recently held “Blessings Boutique” where the public could come to donate and to freely take what they need).

I need transportation to get to-and-from places. That one is a bit tricky but I just purchased a Honda Civic for $4,000 (only 120k miles).

We are getting into the weeds of this post and I thank you for forcing me to clarify my thoughts right here in the comments section for all to see.

Let it be known that Steve Stewart takes things for granted and realizes he has been blessed beyond measure. I will play my part of generous giver and won’t be placing my neighbor into bondage with personal loans or through Peer-to-Peer lending sites so I can get a better ROR.

I hope others will join me in becoming debt free so we can give more.