Choosing a qualified retirement account

I don’t have the benefits of getting a match or having someone contribute to a pension plan in my name. Most people who are in my situation have two great options to choose from: A Traditional IRA or a ROTH IRA. How did I decide between the two? It was easy, I decided to pay for the seed!

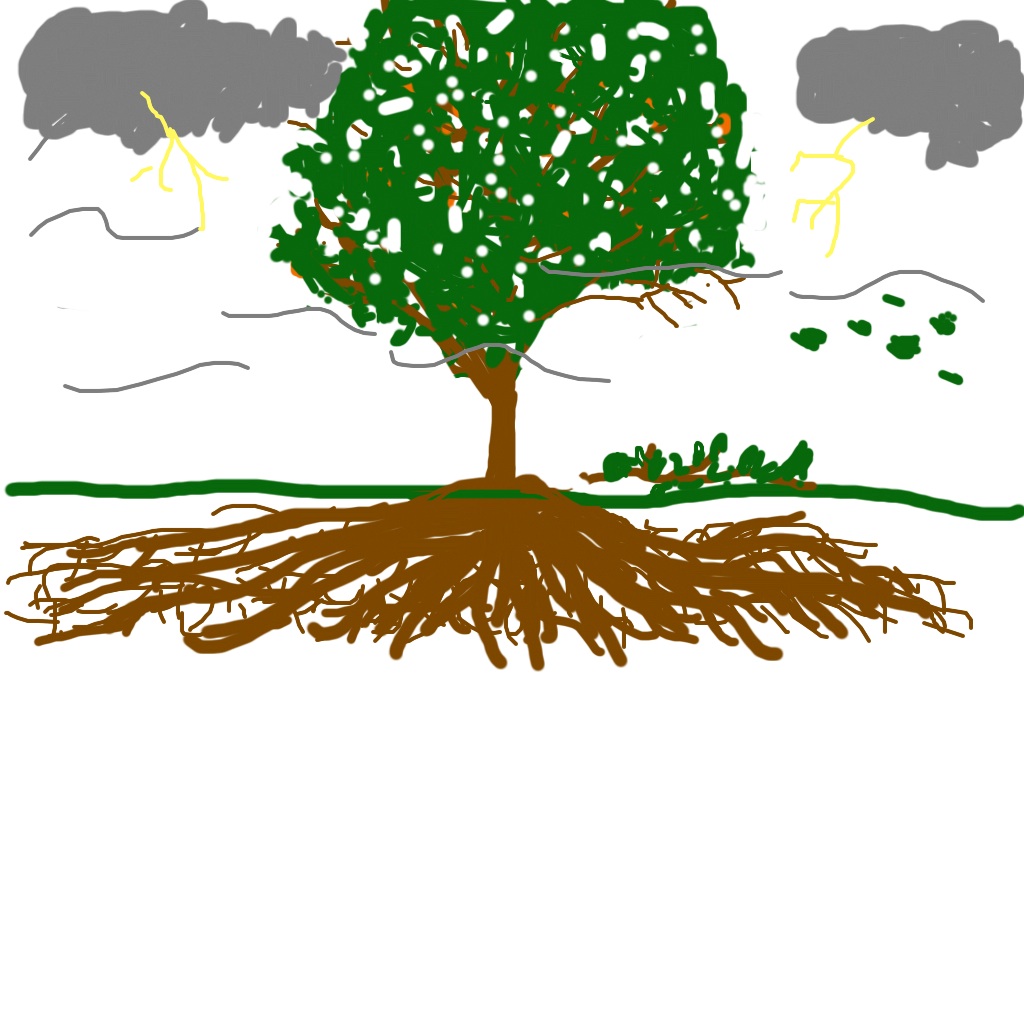

Retirement Accounts are like Trees

Retirement Accounts are like Trees

Picture a retirement account as growing a tree. Watering it (putting money into the account) will help it grow. The more you water it, the more it branches out (investing into multiple types of stock/bond/mutual funds). It also grows a strong root system.

Weathering the Economic Storms

It takes a long time to grow a tree. The same applies to retirement accounts. If you have been saving for a while then you know there are storms that come from time to time (economic storms). The storms will knock off some branches (investments) but you haven’t lost the entire tree.

The fruit

Not only will the tree grow but the branches will start to grow fruit. This is the same for your Tree-tirement account: The investments start to throw off interest and dividends. Don’t pick the fruit before retirement, let them re-invest to help it grow bigger and stronger! My plan is to save enough that my Tree-tirement should be big enough for me to live off of the fruit without having to cut off any branches.

$100 a month for 40 years grows a BIG TREE

If you were to put $100 into a retirement account every month for 40 years ($48,000 every month for 480 months) and that account earned a 12% return then my Tree-tirement would grow to be worth $1.176 MILLION dollars.

The difference between a Traditional and ROTH IRA

A Traditional IRA lets me deduct contributions from my taxable income as I put money into the account. What that means is that I won’t pay taxes on any of the money ($48,000) as I put it in and will pay the taxes when I take money out when I’m old. That saves me taxes today.

With the ROTH option, I don’t get the tax deduction today. In other words, I put money into the account after it has been taxed. The great news is that I don’t pay taxes on the money when I take it out (the million dollar account).

Pay for the seed or the tree?

The choice was very easy for me once I understood this concept. A Traditional IRA is like paying for the tree because I pay taxes on what I take out (the million dollars).

A ROTH IRA is like the seed: I paid the taxes up front (on the $48,000) and get to pick all the fruit I want without having to pay later (on the million dollars). Now THAT’S what I call Tree-Tirement!

So what would you rather do? Pay for the tree (Traditional IRA) or the seed (ROTH IRA)?

Absolutely love this analogy, and it totally makes sense. I already started with the seed and I’m very glad I did. Definitely better to pay the taxes now, then later when I’m a multi-millionaire (ha, a girl can wish)!